On May 25, 2022, the SEC proposed amendments1 to Rule 35d-1, the fund “Names Rule,”2 (Names Rule Amendments) and, separately, proposed amendments3 to several rules and forms that would require additional disclosure for funds and advisers that consider environmental, social, and governance (ESG) factors in their investment processes (ESG Amendments).

This alert focuses on the requirements that apply to registered investment companies. Please see Seward & Kissel’s memorandum, “SEC Proposes Rules Requiring Enhanced ESG Disclosure for Investment Advisers and Registered Funds” for a discussion of how the ESG Amendments relate to investment advisers.

Names Rule Amendments

Background

Adopted in 2001,4 the Names Rule is designed to ensure that a fund’s name accurately reflects the fund’s investments and risks. To achieve this goal, the Names Rule generally requires that if a fund’s name suggests a focus in a particular type of investment, industry, or geographic region (e.g., “Bond Fund,” “Utilities Fund,” or “China Fund”), the fund must adopt a policy to invest at least 80% of its assets in investments suggested by its name (80% policy). Whether a term used in a fund name fell within the Names Rule has been the subject of extensive commentary during the disclosure review process. In 2020, the SEC requested comment on proposed changes to the Names Rule, noting that the 80% test applies to terms in fund names that suggest a “type” of investment, but not to terms that suggest the fund’s “investment objective, strategy or policies.”5

Proposed Amendments

The Names Rule Amendments would expand the current 80% policy requirement to apply to any fund name with terms that suggest a fund focuses on “investments that have, or whose issuers have, particular characteristics.” The text of the Names Rule as revised indicates that an 80% policy would be required for funds with a name using terms such as “growth” or “value,” or terms indicating that the fund’s investment decisions incorporate one or more ESG factors. The Proposing Release also indicates that the Names Rule could include other terms that historically may have not required an 80% policy (depending on the context), like “global,” “international,” “income,” or “intermediate term (or similar) bond.” In addition, if a fund’s name suggests that its investment focus includes multiple elements, the fund’s 80% policy must apply to all elements.6

While the Names Rule currently provides that a fund’s 80% policy applies at the time of investment (incurrence test) and “under normal circumstances,”7 which allows a fund to determine what constitutes something other than normal circumstances, the Names Rule Amendments would impose a maintenance test (with limited exceptions) for the 80% investment requirement. The exceptions would permit a fund to depart temporarily from its 80% policy under four enumerated circumstances:

- as a result of market fluctuations or other circumstances where the departure is not caused by the fund’s investment decisions;

- to address unusually large cash inflows or redemptions;

- to take a position in cash and cash equivalents or government securities to avoid a loss in response to adverse market, economic, political, or other conditions; and

- to reposition or liquidate a fund’s assets in connection with a reorganization, to launch the fund, or when a fund has provided notice to shareholders of a change in the fund’s 80% policy in accordance with the Names Rule.

The Names Rule Amendments specify that a fund departing from the 80% investment requirement pursuant to one of these exceptions must bring its investments back into compliance as soon as reasonably practicable, providing a maximum period of departure of 30 consecutive days, other than in the case of a fund launch (period of 180 consecutive days), a reorganization (no express time limit provided in proposed rule) or where the fund has provided notice it intends to change its 80% policy (no express time limit provided in proposed rule). This time frame for compliance is markedly shorter than the process by which most advisers bring funds back into compliance with 80% policies.

The Names Rule Amendments also address the way funds that use derivatives measure compliance with the 80% test. For example, if applicable, a fund would be required to use a derivatives instrument’s notional value, rather than its market value, to determine the fund’s compliance with its 80% policy.8 The Proposal reflects SEC concerns about the scope of funds’ use of derivatives generally, and that market value may not accurately reflect the investment exposure created by a derivatives instrument.

Other key proposed requirements under the Names Rules Amendments are highlighted below:

Additional Prospectus Disclosure Defining Terms Used in Fund Name. For funds that have to implement an 80% policy, the Names Rule Amendments would require each fund to disclose in its prospectus what the term or terms used in its name mean, including the criteria the fund uses to select the investments the term suggests. A fund may use a reasonable definition of terms used in its name, but the definition must be consistent with its plain English meaning or established industry use.

Using ESG Terminology in a Fund’s Name. Under the Names Rule Amendments, an “integration fund” would be prohibited from using ESG terminology in its name. The Proposing Release describes an “integration fund” as a fund that considers ESG factors in conjunction with other, non-ESG factors in the fund’s investment decisions, but whose ESG factors are generally not significant enough to be determinative in deciding to include or exclude any particular investment in the fund’s portfolio (also, see Proposed Fund Disclosures – Integration Funds below). For purposes of this restriction, terms connoting ESG factors include words like “sustainable,” “green,” “ethical,” “impact,” or phrases like “good governance” or “socially responsible investing.”

Updated Notice Requirements. The Proposal would update the Names Rule’s notice requirement to expressly address funds that use electronic delivery methods to provide information to their shareholders.9 As with the current Names Rule, a fund must provide notice to shareholders at least 60 days prior to a change in its 80% investment policy (assuming that the 80% policy is not fundamental). The Proposal would require funds to prominently identify the notice as an “Important Notice Regarding Change in Investment Policy.”

Form N-PORT Amendments. Registered investment companies, other than money market funds, would be required to report on Form N-PORT the value of the fund’s 80% basket10 as a percentage of fund assets, and, if applicable, the number of days the value of the 80% basket fell below 80% of the value of the fund’s assets during the reporting period. Funds would also identify which investments are included in the 80% basket. This information would be publicly available for the third month of each fund’s quarter.

Recordkeeping Requirements. The Names Rule Amendments would impose additional recordkeeping requirements for funds. A fund required to maintain an 80% policy would be required to keep records documenting its compliance with the rule, including the fund’s record of which investments are included in the fund’s 80% basket, the reasons for any departures from the 80% policy, and the dates of any departures from the 80% policy. A fund that is not required to maintain an 80% policy would be required to keep a record of its analysis that it is not required to maintain an 80% policy.

ESG Amendments

Background

The SEC explained that the ESG Amendments proposal comes as a response to increased investor demand for ESG products and strategies as well as significant variations in how advisers and funds define ESG terms and employ data and criteria as part of ESG strategies. While funds and their registered advisers are subject to general disclosure requirements that cover certain ESG-related investment strategies, there are currently no specific requirements covering what a fund or adviser following an ESG strategy must disclose. The ESG Amendments seek to fill this gap and provide clear and comparable information about how funds and advisers consider ESG factors in their investment processes.

Proposed Amendments

If adopted, the ESG Amendments would impose additional, specific ESG disclosure requirements in fund registration statements and fund annual reports.

Proposed Fund Disclosures

Under the ESG Amendments, a fund engaging in ESG investing would provide additional detail about the fund’s implementation of ESG factors in its principal investment strategies. The depth of required disclosure would depend on how central ESG factors are to a fund’s strategy. The Proposing Release defines three types of ESG funds: “Integration Funds,” “ESG-Focused Funds,” and “Impact Funds.”

Integration Funds. Integration Funds are funds that consider one or more ESG factors alongside other non-ESG factors in their investment decisions, but do not give the ESG factors greater weight than the non-ESG factors. An Integration Fund would be required to describe concisely how it incorporates ESG factors into its investment selection process and which ESG factors it considers. Open-end funds would provide this disclosure in the fund’s summary prospectus, and closed-end funds would provide this disclosure in the prospectus’s general description of the fund. This concise disclosure would be accompanied with a more detailed description of how a fund considers ESG factors in an open-end fund’s statutory prospectus, or later in a closed-end fund’s prospectus. In addition, if an Integration Fund considers Greenhouse Gas (“GHG”) emissions as an ESG factor, the Integration Fund would be required to describe how it considers the GHG emissions of its holdings, including a description of its methodology.

ESG-Focused Funds. An ESG-Focused Fund is a fund that “focuses on one or more ESG factors by using them as a significant or main consideration (1) in selecting investments or (2) in its engagement strategy with the companies in which it invests.” This would include, among others, funds that track an ESG-focused index or apply a screen to include or exclude investments based on ESG factors, and funds that vote their proxies and engage with management of their portfolio companies to encourage ESG practices or outcomes. Expressly included in the definition of ESG-Focused Fund is (1) any fund with a name that indicates the fund’s investment decisions incorporate one or more ESG factors, and (2) any fund whose advertisements or sales literature indicate that the fund’s investment decisions incorporate one or more ESG factors by using them as a main or significant consideration in selecting investments.

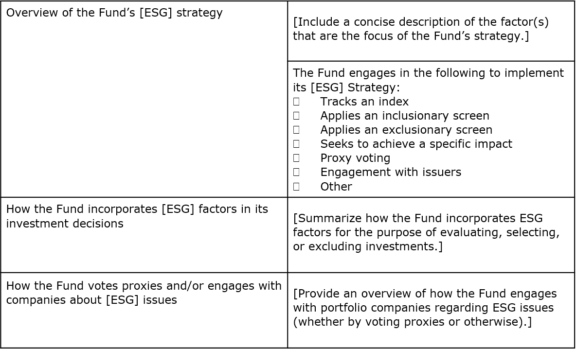

ESG-Focused Funds would be required to provide additional disclosure regarding their ESG considerations in the following tabular format:

[ESG] Strategy Overview

An open-end fund would be required to provide this table at the beginning of its “risk/return summary,”11 while a closed-end fund would provide the table at the beginning of the discussion of the fund’s organization and operation. In addition to the above, an ESG-Focused Fund would be required to provide more detailed disclosure on the items covered in each row of the table later in the prospectus.

Impact Funds. An Impact Fund is a subset of ESG-Focused Funds that seeks to achieve a specific ESG impact(s) – e.g., financing the construction of affordable housing units or advancing the availability of clean water. In addition to the proposed disclosures for ESG-Focused Funds, an Impact Fund would be required to disclose in the “How the Fund incorporates [ESG] factors in its investment decisions” row of the above table, how the fund measures progress towards the specific impact; the time horizon the fund uses to analyze progress; and the relationship between the impact the fund is attempting to achieve and the fund’s financial returns. This disclosure would be supplemented by a more detailed discussion later in the prospectus.

Proposed Fund Annual Report Disclosure

The ESG Amendments would require that fund annual reports provide additional ESG-related information for ESG-Focused Funds and Impact Funds. These proposed disclosures would be included in the management’s discussion of fund performance (or management discussion and analysis, if applicable) section of the shareholder report. The disclosure requirements vary based on the type of ESG Fund and whether the fund votes proxies or engages with portfolio companies on ESG issues.

If adopted, Impact Funds would be required to summarize the fund’s progress on achieving its impact in both qualitative and quantitative terms, and describe the key factors that materially affected the fund’s ability to achieve its stated impact.

ESG-Focused Funds that use proxy voting as a significant means of implementing its ESG strategy would need to disclose information relating to how it votes proxies on ESG-related matters, including the percentage of ESG-related votes cast by the fund in furtherance of an ESG initiative that the fund considers in its investment decisions. In addition, if engagement with portfolio companies on ESG matters is effected through means other than proxy voting, a fund would have to describe progress on any key performance indicators of such progress, including the number or percentage of issuers with which the fund held ESG engagement meetings and the total number of ESG engagement meetings.

Any ESG-Focused Fund that considers environmental factors in its investment strategies would be required to disclose information regarding the GHG emissions associated with their investments, including the carbon footprint and weighted average carbon intensity of its portfolio.

Form N-CEN Amendments

The ESG Amendments would amend Form N-CEN for the purposes of collecting ESG-related information in the structured data language of those forms.

Form N-CEN would be amended to require reporting of information such as: (1) whether the fund uses an integration, focused, or impact strategy; (2) whether the fund considers environmental, social, governance, or a combination of those factors; (3) whether the fund considers ESG information or scores from ESG consultants or other ESG providers; and (4) the name of any third-party ESG frameworks the fund follows.

Comment Period

The comment period for both the Names Rule Amendments and the ESG Amendments will end 60 days after publication of the proposals in the Federal Register.

S&K Observations and Insights

The SEC has expressed significant concerns about the potential of “greenwashing”12 to mislead investors, particularly in light of the substantial growth of ESG funds in recent years. The SEC believes that regulatory action will help address these concerns, specifically by establishing disclosure requirements and a common disclosure framework that makes it easier for investors to understand, evaluate, and compare ESG Funds. But the Names Rule Amendments and the ESG Amendments, if adopted, would have pronounced compliance and disclosure impacts, so we expect that the SEC will receive a significant number of comments on both proposals.

We note, among other things, that the proposed change to the Names Rule to include names suggesting an investment focus would drastically expand the current reach of the rule; it would capture fund names that include terms (beyond those referencing ESG) that have historically not required an 80% policy, such as “growth,” “value,” and “international.”13 Furthermore, the proposal to transform the 80% investment requirement from an incurrence test to a maintenance test (with limited exceptions) could have profound effects on portfolio management and introduces a level of compliance monitoring beyond that which many firms are accustomed to in the context of investment policy compliance. The Names Rule Amendments would also impose new and fairly onerous recordkeeping requirements, including with respect to determinations on whether portfolio holdings comply with a fund’s 80% policy.

While the SEC has not proposed a specific definition for ESG, or for ESG factors, the ESG Amendments include a significant number of specific requirements covering what a fund following a particular ESG strategy must disclose. Compliance with some requirements may be time-consuming and challenging, such as the requirement for Impact Funds to disclose detailed information on metrics to assess their progress and for certain ESG-Focused Funds to disclose information on GHG emissions.